Extortion, Valuation Manipulation, and Rigging The System: How America Plays the Monopoly Game

Extortion, Valuation Manipulation, and Rigging The System: How America Plays the Monopoly Game

It Took a 2 Week Vacation To Bring America To Its Knees

It Took a 2 Week Vacation To Bring America To Its Knees

Since the start of this COVID conundrum — back when it was first starting as rumors and SitRep leaks coming out of Wuhan — I’ve been slamming the table (along with many others) and kicking and screaming to everyone around us that the system is f*cked, and not ready to handle the load that is going to be applied to it.

NOW, disclaimers:

I’m not an economist, market analyst, sociology or what-have-you degree graduate or established expert

My degree is in health, and specifically Exercise & Movement Science

I’m by all means a hobbyist, and I’ve only been paying attention for a short while

If you’re comfortable with knowing those facts and still curious about my input and why — please continue. I will attempt to include all cited sources on the information that I’m drawing my conclusions off of (there’s a lot).

By suppressing the value of the gold-backed-dollar (done by increasing the value of gold vs the dollar), this allowed FDR to prop up the valuations of the gov’t’s gold reserves. Propping the valuation of the stockpile from $4 billion to $7.35 billion.

Our economy isn’t just failing… it’s flailing. The economy is being brought to its knees right now, for multiple reasons; healthcare as a for-profit system, lopsided outsourcing of labor, missteps in leadership… and the [Just-Enough] supply-chain system (that not only the U.S. but many developed countries around the world have been practicing for the past decades) is shooting us — as a country, and as a unified people — in the knee.

Meanwhile Keynesian Economics, defined by Investopedia as: “optimal economic performance could be achieved — and economic slumps prevented — by influencing aggregate demand through activist stabilization and economic intervention policies by the government, is wreaking havoc on our system because it was practiced unabated, and unchecked” — which can be found here. This allowed for spending and borrowing to run rampant while punishing individuals saving and holding cash.

Fractional Reserve Banking (FRB)has been allowing banks to put the money in their care to work to earn more money for themselves, initially a good thing. Banks making profits allow them to stay on top of their system integrity and security. BUT, these banks have been allowed to loan out 90–97% of the money that their clients are keeping with them. Now this pandemic those guidelines have been adjusted to 100%.

And this starts the rabbit hole…

Positions of power always get gameified and manipulated by those who seek power most

Gold Standard

The reason that FRB is capable of even being practiced points to gold. I’ll put up a summarized quick timeline here:

1933: bank-runs on gold reserves at the Federal Reserve Bank

1933, April 20: FRD ordered citizens to turn in their gold for USD. This gold was hoarded at Ft. Knox; largest gold supply in the world (at the time). (This is a literal case of the gov’t extorting and taking advantage of the citizens it claims to protect with the intention of stealing wealth from their population.)

1934: Gold Reserve Act: prevented private ownership of gold, except under license — this allowed the US Government (gov’t from here on out) to pay their debts (bonds) in USD instead of gold. This act also allowed FDR to suppress the value of the gold-dollar by 40% (how in the f$#@ is this legal). By suppressing the value of the gold-backed-dollar (done by increasing the value of gold vs the dollar), this allowed FDR to prop up the valuations of the gov’t’s gold reserves. Propping the stockpile from $4 billion to $7.35 billion. After jacking up the gold valuation, it ended up suppressing the value of the dollar by 60%. (So the United States forced citizens to turn over their gold, acquired and hoarded it all, then propped up its value so that the gov’t could have a fatter wallet. In what world does that sound legal to any of you?)

1944: Bretton Woods Agreement: 44 Countries at the United Nations Monetary & Financial Conference; Gold was the backing for the dollar, while other foreign currencies were pegged to USD. These countries agreed to not allow diversions of valuation against the dollar by more than 1%, meaning; if a country’s dollar became too high vs USD, the host country would print more of their currency and devalue it by increasing the circulating supply, and if it fell too low it would be purchased from the monetary exchange. This agreement allowed trade to be settled in USD instead of gold (which is difficult and costly to physically transport and trade), and thus increased the value of the dollar without affecting the price of gold. (Price Manipulation, to try and make sure that other countries cannot gain any value against the US Dollar, while not affecting the value of gold.)

1960: US held; $19.4B in gold reserves + $1.6B the IMF, enough to cover $18.7B in foreign dollars outstanding.

1970: US held only $14.5B in gold, against a WHOPPING $45.7B in foreign dollar holdings (a little lopsided on the balance sheet there). President Nixon prevented the Federal Reserve from redeeming dollars for gold.

1976: Nixon suspends the Gold Standard — causing the dollar to be backed by itself. THE DOLLAR IS BACKED BY ITSELF. THAT DOESN’T MAKE ANY SENSE. Now, this was intended to be a temporary tactic. Once this happened, and gold was traded in a free market, it tripled from $42 to $124 per ounce.

2011, September 5: Gold was priced at $1895 per ounce.

Taking the dollar off a basis-point that is centered around a deflationary and limited supply, opened up the capability and temptation to just print money for whatever the Fed deems necessary.

This capability of future mishandling is a virtual certainty when humanity is involved. Positions of power (and the authority to print money is absolute power in today’s age) always get gameified and manipulated by those who seek power most….

History has shown that paper monies have failed EVERY SINGLE TIME. The system was first put in practice by the Chinese during the Song Dynasty in the 12th century, called the jiaozi. This first paper note failed as the Song fell to the Mongols. Following this, the Mongol Yuan (established by the Mongols, with the same intent of currency with capable & complete control over its issuance) was not backed by silver nor gold, and quickly ran into a situation of runaway inflation, leading to the collapse of the dynasty in 1368. And then again with the famous Fall of Rome, catalyzed by Rome chipping their gold coins to stretch the supply of their reserves… ultimately debasing their currency. The longest standing fiat currency? The British Pound Sterling; at over 300 years old, and even it has been devalued by nearly 99% of its original value.

Humanity has shown that when it comes to money, we are not responsible enough to keep greed and irrationality out of the conversation.

Debt-Based Economy & Credit

Banks offer reward for holding savings accounts on their balance sheets by paying an interest rate on savings accounts. This is because these banks are utilizing your funds to issue loans and capitalize on these Assets Under Management (AUM), which is part of the FRB system.

But interest rates have been absolutely negligible for any Average-Joe citizen, which are at 0.09% APY according to Smartasset.com which can be read here. As a visual representation that is (0.0009) in decimal, 1% would be (0.01). That means if you held $10k in a savings account, you would earn a piddly ($9.00). Uhhhhhh… yeah you won’t see me holding any significant capital on any savings account, which US Bank’s rate is (0.01%). MEANWHILE, most of our banks are charging “maintenance fees” on our virtual accounts. So with these negligible interest earnings and consistent fees monthly/quarterly, you’re not making money. You’re losing money, and likely hemorrhaging without realizing because the amount you’re passively putting in is still covering up these costs.

So the banking system is punishing the average American for saving money, and motivating that same individual to spend, spend, SPEND. Because increased spending makes for a healthy economy right? Wrong, this Keynesian economics practice is showing it’s weakness today. The over-spending and under-saving causes for a huge exposure in those practicing this style when emergencies arise.

While America was busy spending like it was going out of style, they didn’t realize that the slightest hiccup in the system will cause the world that they built on stilts to come crashing down around them….

Survey: 69% of Americans Have Less Than $1,000 in Savings

Despite a strong economy, a majority of Americans seem to be struggling to save money, according to GOBankingRates'…www.gobankingrates.com

Further, according to ^^ those statistics, the average American is F*CKED if any sort of emergency were to happen. How many issues can you conceive that would amount to $1000 or more? It’s a lot. What’s the main reason for this abysmal statistic? The majority are living paycheck to paycheck without the ability to put money aside.

I will point out more on this problem as we go. But so far we have;

The dollar is backed by nothing but trust that the US gov’t will act in best intention for the average American, which we’ve seen time and time again that those in power do not.

The economy is addicted to spending, and punishing individual savings.

Americans are by-in-large living paycheck to paycheck and cannot afford to put money aside with the desire to increase their individual wealth.

Small Business Copying Big Business

The American Dream; forge your own path, start your own business and increase your wealth and take part in the free market.

Small businesses are being pressured to spend like the individual; don’t save, spend. Don’t stockpile, produce just enough to keep supply chains constantly running, busy and working. Reduce time-on-shelf retail ratios. And that’s not to mention the benefits large businesses receive with bulk manufacturing & production.

We’ve got small businesses spending their souls away to make profits, being punished for saving any cash on the side for emergencies and planning things out to run out of stock just in time for the next shipment to arrive.

And what’s happening now? Entire countries across the globe are stopping all activities. Small businesses cannot get money from their business practices, and cannot afford to pay their own employees and rent.

Big Business Bailouts & the Small Sales Slaughterhouse

“How can you say the economy is in a bad spot? The S&P 500 just had it’s largest green day ever.”

Stocks going up is not indicative of the economy being healthy. In regards of the ^^above statement, I suggest you look at a technical analysis term called a “dead-cat-bounce.” Stocks can very easily go up (and up rapidly, albeit momentarily) during a market downturn for multiple reasons; seller exhaustion, stock buybacks, speculation, short-term reaction to news/rumors/hope. Aside from those small reasons, real economic ramifications are swift on paper but very slow and drawn out in reality. As employees lose jobs, and the capability to pay on memberships, utilities, rent, food… things get ugly fast.

We’ve been finding out that large-scale businesses and corporations have mismanaged their money on such a catastrophic level that these “professionals” are incapable of funding their employees’ salaries for a 14-day shutdown. While these large companies were irresponsible, and refused to prepare for an emergency… they err’d on the side of just not wanting to think about a possible bad moment occurring. Clearly as long as you don’t think about a bad thing happening, it doesn’t happen, right?

14 DAYS AND THE US ECONOMY CRUMBLES.

These large businesses will receive their bailouts at lightning fast speeds (in an effort to avoid them making a large impact on unemployment numbers) while using this free money to also position themselves aggressively within the market. We watched it happen in 2008, we’re about to watch it happen again. All while your local businesses will be left with their hands out, waiting for the assistance to take it’s time to get to the local community level, and you/your family/your neighbors will be stuck watching as the larger players (i.e. national banks, Apples, Walmarts, etc.) swoop in demanding their payments, and gobbling up these businesses while the average American bleeds out onto the streets.

Bailing out these industries AGAIN, after 2008, is only rewarding their behavior. If these companies were allowed to die, it would cleanse the market of bad-actors and allow for the capital to flow directly to the best businesses with wise leadership and profitable plans.

Where Are We Now?

Okay so the dollar is being printed into oblivion.

We’re living on a paycheck to paycheck basis.

The banking system is applying pressure to spend everything you earn (in the false belief that it will reward everybody).

The banking system is also punishing us for saving with them.

We’re being suggested to take on debt so that more debt can be added to the system.

UHHHH… correct me if I’m wrong but that sounds like a massive ponzi scheme.

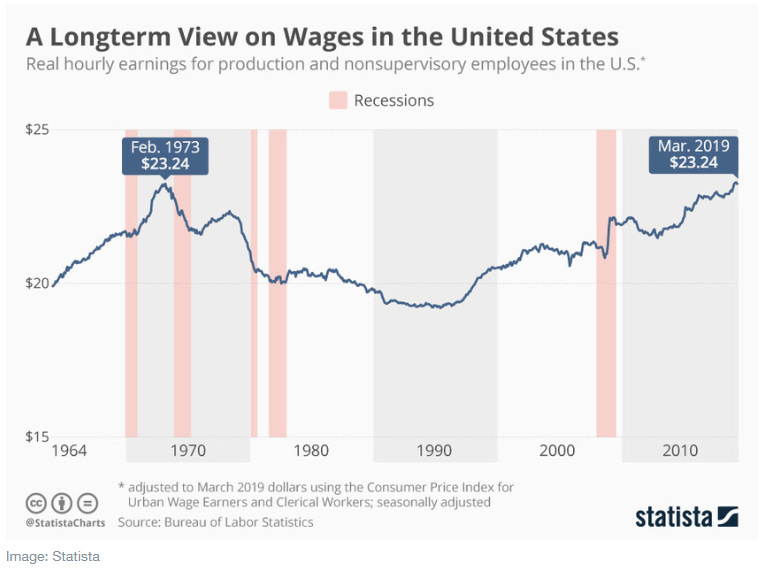

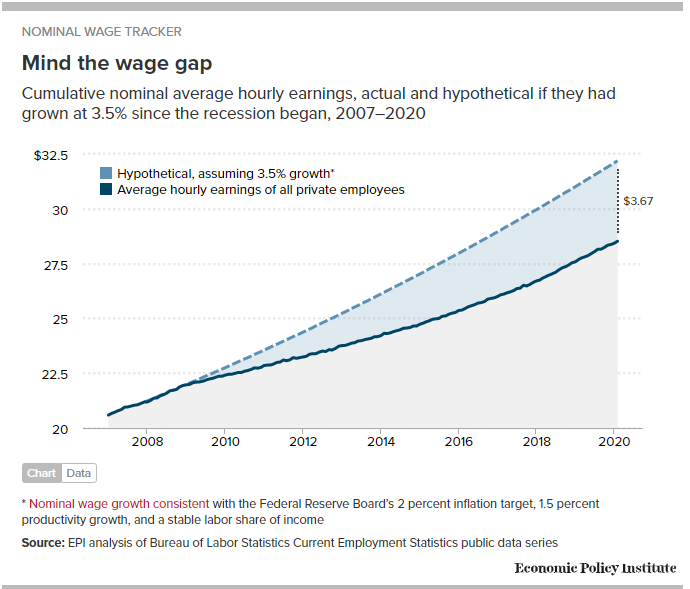

AND we’re just barely back to average hourly wages being equal to that of the dollar from 1973. I don’t know about you guys, but I would think that the average hourly earnings should be a bit higher than that considering how much more expensive everything else in our lives is.

Good point, lets compare those numbers….

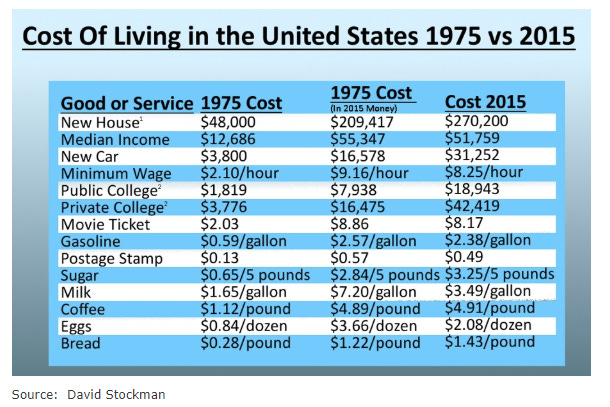

Price Inflation & Purchasing Power

Just how ugly is the cost of living today? Well, I couldn’t find numbers for precisely up to 2019, but I’ve found some data for within the past few years — close enough.

Now, as far as all things that I’m speaking on — I’m out of my element here, I’m not an expert. And I’m DEFINITELY not someone to explain the data ^^above. But, I can tell you that if you do the math to account for the average rate of inflation, you can get back to how much purchasing power the dollar back in 1975 had. And that’s how they’re basing this data in the chart. As far as inflation and American living standards go… the big problem areas are the areas where every American was pushed to go in their years of youth; go to college, buy a home, own a car — live the American Dream. All 3 of those are based on credit, and debt. And they’re MASSIVELY bubbled. Holy sh*t I mean look at the rate of inflation that happened in 40 years. That is absolutely absurd.

Those individuals are also expected to have a profitable lifestyle, reproduce, and raise children to be constructive members of society. Kinda hard to do that when you’re stressing about your debts, can’t get a decent job because the market is over-saturated with college graduates all competing for the same position, and then wages haven’t increased in tandem with inflation.

Now I am in no position to examine this further because it is probably the furthest outside of my understandings of any of the workings of these systems. The link to look at more data like that to the left can be found here.

Demographics

The last portion of this I’ll leave on is demographics. Mark Yusko is an absolute wealth of knowledge, and I believe has experienced plenty of market deviations to have a logical outlook on the current situation as well as be willing to acknowledge new ways of thought and progressing technologies. Which both are advancing rapidly in our era.

Mark brings up a few good points in his conversation with Anthony Pompliano on a few things that are happening seemingly, behind the scenes… but very much potent in the effect. First is the pension epidemic, according to their information the vast majority of pensions in America are under-performing. From my understanding this is because they were seeking secondary revenue streams in an attempt to increase returns and beat the market further. While the market had reached a massively over-extended point in this bull-market and investors and fund managers likely became complacent and relaxed thinking our market’s riches will never end. If pensions can’t pay out what they’re promising to their constituents upon retirement that’s going to leave a lot of Americans in very bad positions.

On top of pensions not being capable of paying their dues, those same individuals retiring will be cashing out their retirement plans and pulling funds out of the market to subsist off of during their well-earned hiatus’ at the ends of their lives. That also means even MORE funds leaving the market that were previously holding the market up.

Retirees are on the rise in their ranks, while births are declining and our young generations aren’t capable of affording frivolous spending or even realistically spending on essentials without digging themselves a grave made out of debt that only piles-on and barely chips away. That all adds up to a negative return.

OKAY. So in conclusion;

America manipulated its citizenry to steal their gold reserves

Hoarded and adjusted the pricing of gold after the heist, to increase profit

Decoupled the dollar from gold reserves sending it free-floating in valuation

Rigged the valuations of other currencies to prevent other countries from gaining against the USD

The decoupling allowed the Federal Reserve to print at their heart’s content

The unlimited money printer allowed stocks to become highly over-priced

Central Banks pushed American Citizens and American Businesses to spend beyond their means, and take on more debt then they’re realistically capable of servicing

Banks punish American Citizens for placing money in savings accounts with laughably minute interest rates, all while charging them for even holding funds in these accounts through hidden fees

Big Business gets continuously bailed out for making stupid decisions, and then using the funds to pull their money from the market and then purchase small business that bleed into bankruptcy, increasing their market share of control indirectly

Cost-of-living has inflated out of control

Wages have not been kept up to the rapid pace of inflation

Population growth rate is negative

Retirees are pulling funds from the system through social security, under-funded pensions, IRA’s and 401ks being cashed out

All while everyone in charge telling American that’re none-the-wiser that “everything is fine” and the system has “never been better.”

Wake up. Pay attention in reality and stop just taking media headlines and news at face value. There’s a cancer at the center of America and her economy.

Thank you for your attention. Stay safe, stay healthy.

If you enjoyed reading please check out my follow up piece also featured in CoinMonks here.

References:

Spotify:

Tales From The Crypt; hosted by Marty Bent & Matt Odell

The Pomp Podcast; hosted by Anthony Pompliano

Online Sources:

Amadeo, Kimberly. “Is Your Credit Card Debt Higher Than Average?” The Balance, The Balance, 11 Mar. 2020, www.thebalance.com/average-credit-card-debt-u-s-statistics-3305919.

Amadeo, Kimberly. “When the Dollar Was Backed By Gold.” The Balance, The Balance, 21 Feb. 2020, www.thebalance.com/what-is-the-history-of-the-gold-standard-3306136.

Emmiemartin. “Home Prices Have Risen 114% since 1960 — Here’s How Much More Expensive Life Is Today.” CNBC, CNBC, 17 Apr. 2018, www.cnbc.com/2018/04/17/how-much-more-expensive-life-is-today-than-it-was-in-1960.html.

Kagan, Julia. “Fractional Reserve Banking.” Investopedia, Investopedia, 29 Jan. 2020, www.investopedia.com/terms/f/fractionalreservebanking.asp.

Pritchard, Justin. “How Does Fractional Reserve Banking Affect Your Savings?” The Balance, The Balance, 28 Aug. 2019, www.thebalance.com/what-is-fractional-reserve-banking-4590236.

Szczepanski, Kallie. “The Invention of Paper Money in China.” ThoughtCo, ThoughtCo, 17 Oct. 2019, www.thoughtco.com/the-invention-of-paper-money-195167.